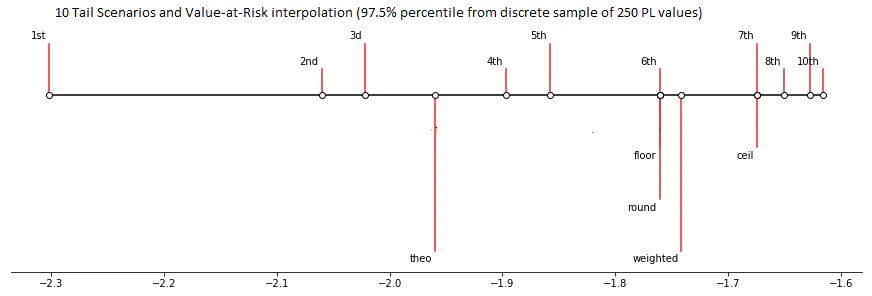

| Floor | Simulated PL for the lower of the adjacent ranks | VaR = PLlower | For x = 6.25, the PL value at rank 6 is taken as the VaR. | |

| Ceil | Simulated PL for the higher of the adjacent ranks | VaR = PLhigher | For x = 6.25, the PL value at rank 7 is taken as the VaR. | default option |

| Weighted | Simulated PL linearly interpolated between the adjacent ranks | VaR = weight∗PLlower+(1−weight)∗PLhigher | For x = 6.25, the linear interpolation beween PL value at rank 6 and PL value at rank 7 at the point x = 6.25 is taken as the VaR. | |

| Round | Simulated PL for the nearest rank | VaR = PLnearest | For x = 6.25, the PL value at rank 6 is taken as the VaR. | |

| | | For x = 6.75, the PL value at rank 7 is taken as the VaR. | |

| | | For x = 7.5, the PL value at rank 8 is taken as the VaR. | |

| | | For x = 8.5, the PL value at rank 9 is taken as the VaR. | |

| | | For x = 9.5, the PL value at rank 10 is taken as the VaR. | |

| Round Even | Simulated PL for the nearest rank with rounding half to even | VaR = PLnearestEven | For x = 6.25, the PL value at rank 6 is taken as the VaR. | |

| | | For x = 6.75, the PL value at rank 7 is taken as the VaR. | |

| | | For x = 7.5, the PL value at rank 8 is taken as the VaR. | |

| | | For x = 8.5, the PL value at rank 9 is taken as the VaR. | |

| | | For x = 9.5, the PL value at rank 10 is taken as the VaR. | |