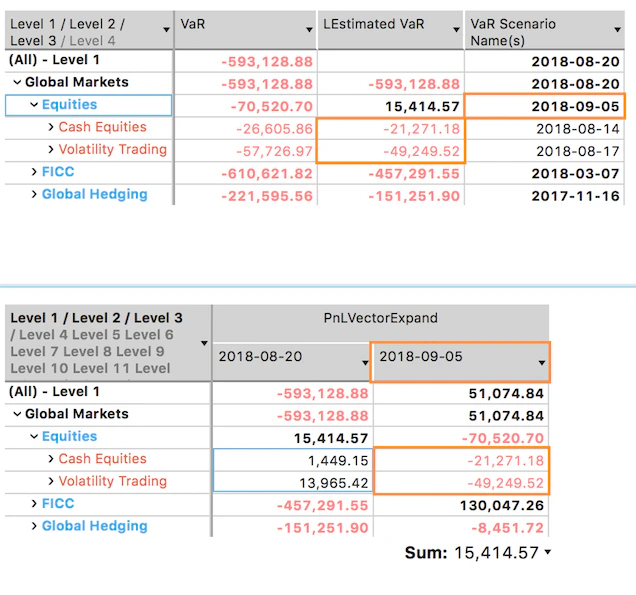

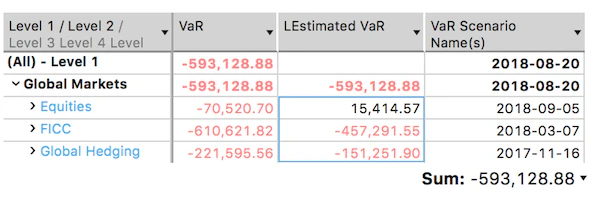

-593k and equals the VaR value computed for the “Global Markets”. Although the VaR Scenario name(s) measure indicates that the VaR scenarios for each sub-portfolio were different, the LEstimated VaR has been based on the total portfolio VaR scenario 2018-08-20.

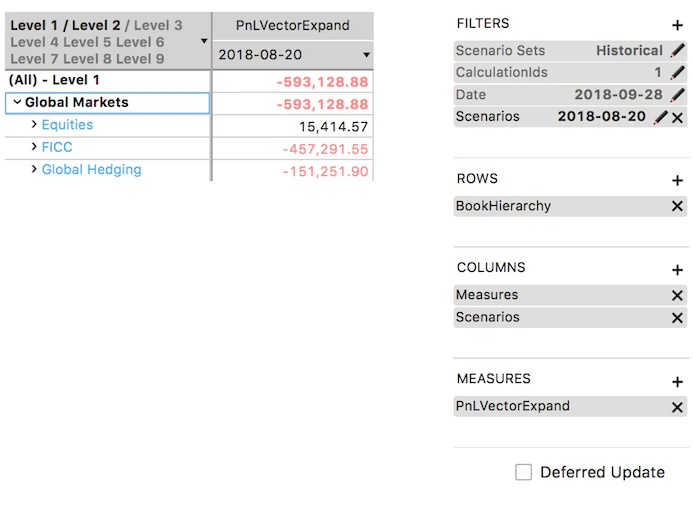

2018-08-20 scenario. Indeed, the simulated PL values for the sub-portfolios match their LEstimated VaR values.

2018-09-05 in our example.