Aggregate capital - Regulatory Calculation

Choice of approach

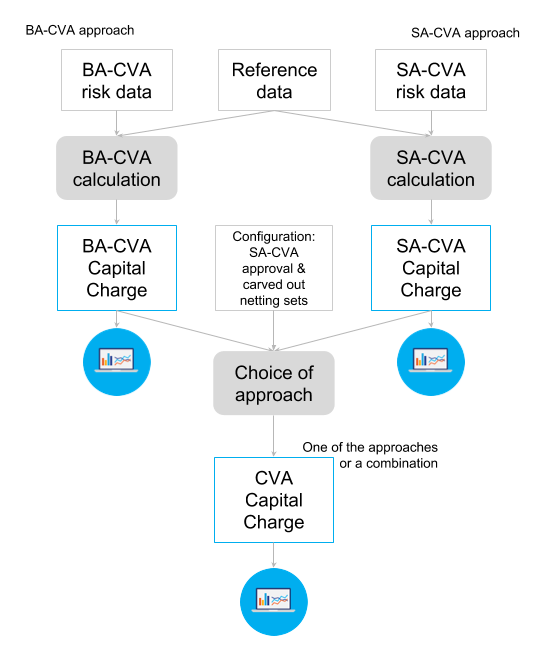

CVA Risk Capital methodology allows capitalizing CVA risks under either SA-CVA or BA-CVA approach - both of them are implemented as measures in Atoti CVA Risk Capital and can be analyzed in parallel in a consistent combined view.

The choice of the method is specified as follows in [MAR50]:

- [MAR50.7] …Banks must use the BA-CVA unless they receive approval from their relevant supervisory authority to use the SA-CVA.

- [MAR50.8] Banks that have received approval of their supervisory authority to use the SA-CVA may carve out from the SA-CVA calculations any number of netting sets. CVA capital for all carved out netting sets must be calculated via the BA-CVA.

Hence the final regulatory capital measure - CVA Capital Charge - may choose either BA-CVA or SA-CVA calculation results or combine them.

CVARC = CVARC BA + CVARC SA, where CVARC BA is BA approach charge for positions treated officially under BA approach and CVARC SA is SA approach charge for positions treated under SA approach.

The capital treatment - ‘SA-CVA’ or ‘BA-CVA’ - for each of the netting sets/trade can be displayed using a hierarchy “CapitalTreatment”.

Capital treatment configuration

The Solution supports time-dependent configuration of the model settings; and the regulatory capital measure may switch from BA-CVA to SA-CVA approach based on the SA-CVA approval obtained.

Availability of supervisory approval to use SA and the list of netting sets carved out from SA-CVA are slow-moving model parameters. They are provided as two csv files in the reference implementation. For more details, please refer to Input Data Files Formats.

See also

- Approval to use SA

- Carved out netting sets

- [TradePosition].[CapitalTreatment]

- [TradePosition].[IsCarvedOut]