Context Values

The confidence level context values (ESConfidenceLevel, ETGConfidenceLevel, VaEConfidenceLevel, VaRConfidenceLevel) can be used to override the default confidence level in their respective calculations.

PercentileBuckets

Controls the number of buckets used by the distribution histograms. If a user changes it to, say, 10, the PnL values are re-bucketed and the distribution charts updated.

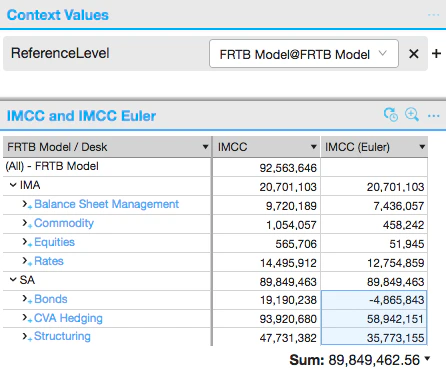

ReferenceLevel

Specifies the cube level at which the capital charge is calculated. Defaults to “Enterprise” (top of house). All capital allocations are relative to the ReferenceLevel. Labels in the selection list read as follows:Desk@Desks— the level “Desk” in the hierarchy DesksLevel 5@BookHierarchy— level “Level 5” in the hierarchy BookHierarchy

euler, pro_rata, incremental.

VaRTimePeriod

Works in conjunction with theLiquidity Horizon field in the Scenario input table. Scales VaR vectors to the specified time period using the Square Root of Time rule.

Example: If scenarios contain both 10-day and 1-day vectors and VaRTimePeriod is set to 1, the 10-day vectors are normalised to 1 day while the 1-day vectors are unchanged.

10-day VaR and 1-day VaR should not be aggregated — Liquidity Horizon should be used as a slicing hierarchy.