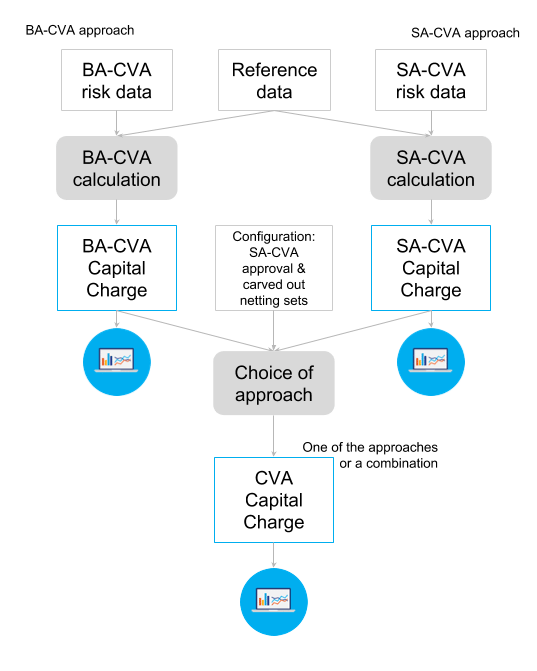

Choice of approach

CVA Risk Capital methodology allows capitalizing CVA risks under either SA-CVA or BA-CVA approach - both of them are implemented as measures in Atoti CVA Risk Capital and can be analyzed in parallel in a consistent combined view. The choice of the method is specified as follows in [MAR50]:- [MAR50.7] …Banks must use the BA-CVA unless they receive approval from their relevant supervisory authority to use the SA-CVA.

- [MAR50.8] Banks that have received approval of their supervisory authority to use the SA-CVA may carve out from the SA-CVA calculations any number of netting sets. CVA capital for all carved out netting sets must be calculated via the BA-CVA.