> ## Documentation Index

> Fetch the complete documentation index at: https://docs.activeviam.com/llms.txt

> Use this file to discover all available pages before exploring further.

# LEstimated measures

> The LEstimated VaR is a contributory measure. It is an additive measure such that the LEstimated VaRs of all Sub-Portfolios add up to the VaR of the parent P...

The LEstimated VaR is a contributory measure. It is an additive measure such that the LEstimated VaRs of all Sub-Portfolios add up

to the VaR of the parent Portfolio.

The LEstimated VaR shows the simulated PL for the tail scenario, that has been identified as the VaR scenario for the parent Portfolio.

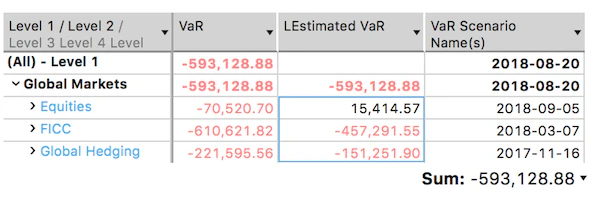

In the screenshot below, a pivot table displays [VaR](../cube/measures/var/value-at-risk) and [LEstimated VaR](../cube/measures/var/value-at-risk). The total of the LEsimated VaRs for the sub-portfolios under the “Global Markets” node is `-593k` and equals the VaR value computed for the “Global Markets”. Although the [VaR Scenario name(s)](../cube/measures/var/value-at-risk) measure indicates that the VaR scenarios for each sub-portfolio were different, the LEstimated VaR has been based on the total portfolio VaR scenario `2018-08-20`.

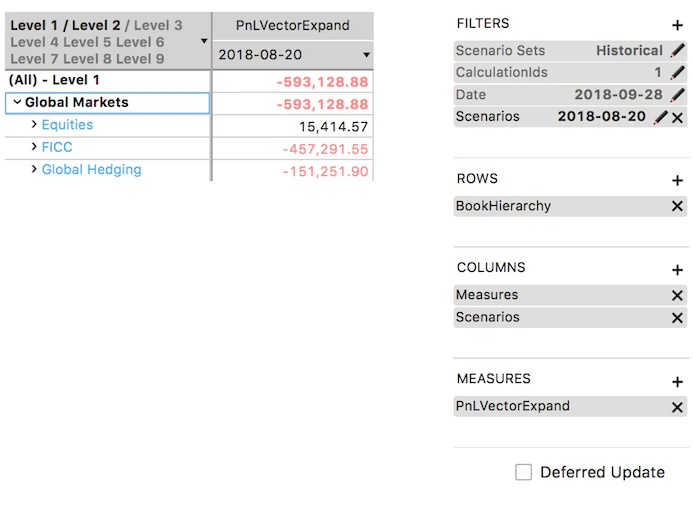

The following screenshot displays the [PnLVectorExpand](../cube/measures/var/technical) measure for the `2018-08-20` scenario. Indeed, the simulated PL values for the sub-portfolios match their LEstimated VaR values.

The following screenshot displays the [PnLVectorExpand](../cube/measures/var/technical) measure for the `2018-08-20` scenario. Indeed, the simulated PL values for the sub-portfolios match their LEstimated VaR values.

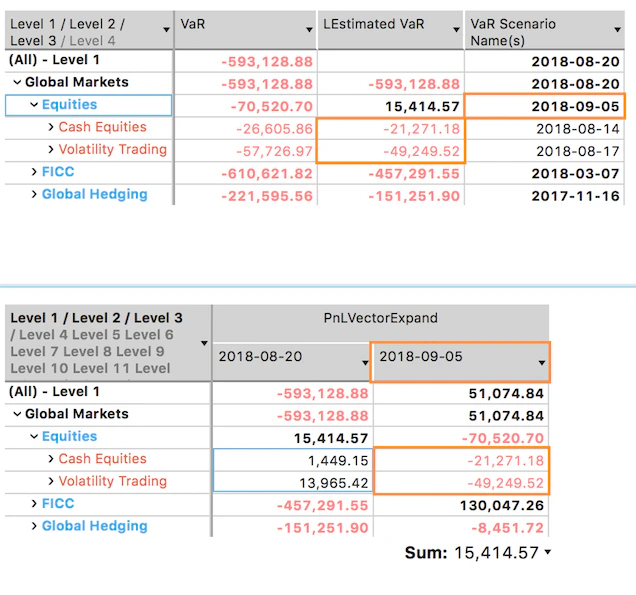

If the BookHierarchy is expanded further, the LEstimated VaR for the Level3 sub-portfolios will match the VaR Scenario computed for the Level2 parent, which is `2018-09-05` in our example.

If the BookHierarchy is expanded further, the LEstimated VaR for the Level3 sub-portfolios will match the VaR Scenario computed for the Level2 parent, which is `2018-09-05` in our example.

## See also

* [Component Measures](./component)

* [Incremental Measures](./incremental)

## See also

* [Component Measures](./component)

* [Incremental Measures](./incremental)